The Ukraine war has global economic ramifications. How do you feel it in the local real estate market? PriceHubble investigated this question with a survey of real estate professionals from all areas of the real estate industry.

55 percent of the real estate professionals who took part in the current study "Effects of the Ukraine War on the Real Estate Industry in Switzerland" believe that the Ukraine crisis could have a negative impact on their company over the next twelve months. 31 percent think there will be no impact. In contrast, 14 percent of respondents see a positive development for their business.

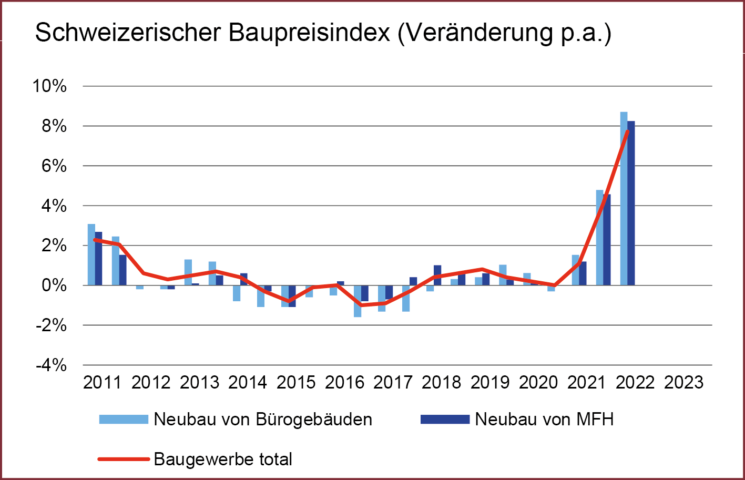

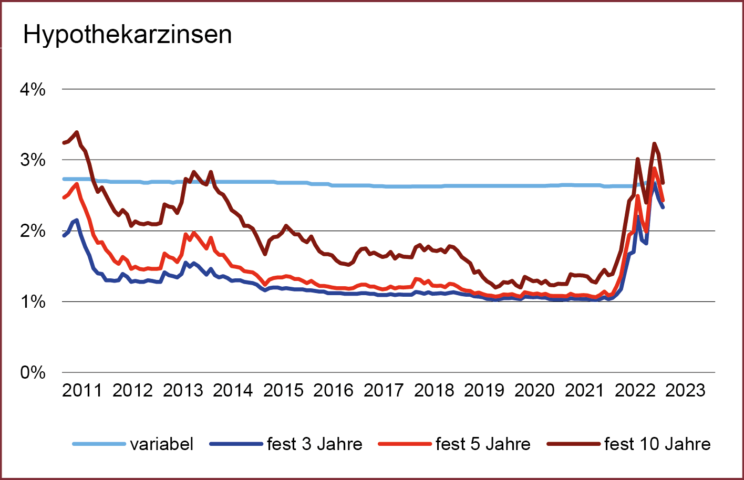

According to those surveyed, the reasons for a change are the increase in construction costs, rising mortgage interest rates and a stagnating or declining buyer's market. As one real estate manager comments: «The increase in material costs and delivery times affects both the construction sites and the purchase prices. As a result, buyers will resort to existing goods and abandon construction projects.”

In general, more real estate professionals (28 percent) see a decrease in the number of mandates over the next twelve months than an increase (17 percent). More than 55 percent of those surveyed do not expect any change in the number of mandates.

50 percent of the respondents are of the opinion that projects will not be postponed because of the Ukraine war. 9 percent expect a postponement of up to 6 months, 12 percent a delay of 6 to 12 months, 26 percent of 12 to 18 months, 2 percent a postponement of the projects by 18 to 24 months and another 2 percent even by up to to 24 to 30 months.

Development of luxury properties difficult to predict

In the case of luxury real estate, 34 percent of those surveyed stated that they expected prices to rise. In contrast, 31 percent believe that a decline is to be expected. 35 percent are of the opinion that the prices in this segment will not change.

In the comments column to this question, many of the respondents indicated that they expected a decrease in general interest in objects in this segment. Others are of the opinion that luxury real estate is crisis-resistant and that the strong demand will remain. Many are also convinced that the supply will remain stable.

"Luxury real estate in Switzerland, especially in exclusive locations, will always tend to find buyers (both domestically and abroad) and it is therefore possible that the prices for them remain the same or may even rise," comments one broker.

Price development of energy-efficient objects remains exciting

When it comes to the question of whether a greater price change is to be expected when buying properties with a high energy efficiency class (A or A+), there is a tie: 50 percent say "yes" and 50 percent say "no".

With regard to the demand for real estate with a high energy efficiency class since the beginning of the Ukraine crisis, 68 percent of the real estate experts surveyed stated that they had not noticed any change. "But it will come, people are slowly becoming sensitive to it," a real estate manager commented on this question. 32 percent of those surveyed believe that demand has already increased.

Regarding rental prices for properties with a high energy efficiency class (A or A+): 69 percent of the participants stated that there will be no changes. In contrast, 31 percent expect a change.

Further results, for example on the impact of rising mortgage interest rates, the development of rents or sales prices of residential properties can be found in the complete study.