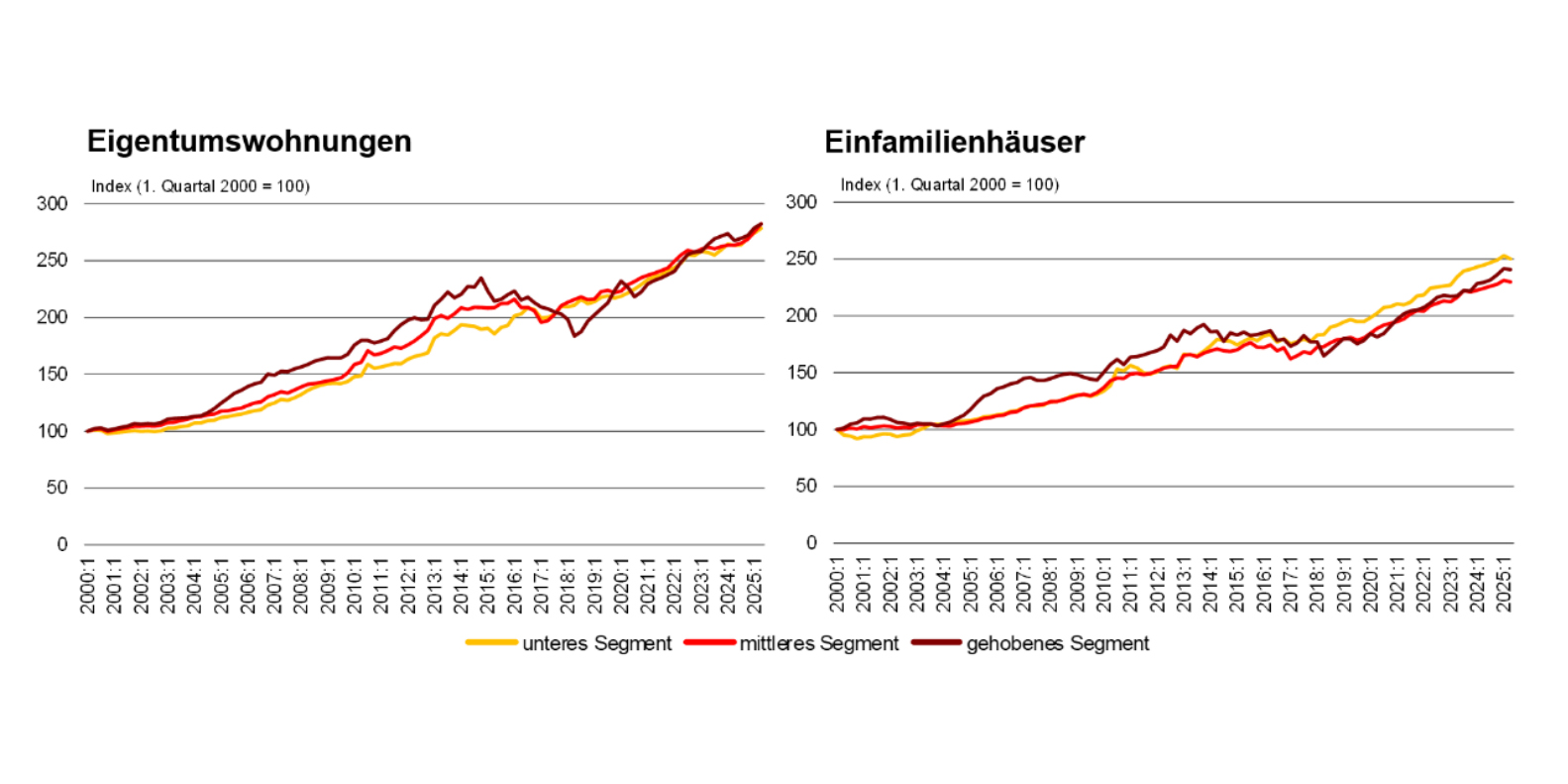

According to the latest analyses by Fahrländer Partner Raumentwicklung (FPRE), prices for condominiums rose by 1.7 per cent in the second quarter of 2025 compared to the previous quarter. The middle segment was particularly hard hit with an increase of 2.5 per cent. The lower ( 1.5 %) and upper segments ( 1.2 %) also recorded price increases. A year-on-year comparison shows significant growth, particularly in the regions of Basel ( 9.1 %), Zurich ( 7.9 %) and southern Switzerland ( 7.7 %).

Single-family homes with stable development The situation is different for single-family homes. Compared to the previous quarter, prices have largely stagnated (-0.6 %). The change in the individual segments remains moderately negative, -1.1 per cent in the lower, -0.6 per cent in the middle and -0.4 per cent in the upper market segment. Over the course of a year, however, the average increase is 2.5 per cent.

Demand exceeds supply The sustained demand for housing continues to be met with restrained construction activity. FPRE therefore expects prices to continue to rise over the next twelve months, both for condominiums and single-family homes. Central locations in particular are likely to benefit more. Stefan Fahrländer, Partner at FPRE, summarises: “The demand for residential property remains high, which is reflected in rising prices in almost all regions of Switzerland.”

Construction activity realised a small year-on-year increase of 0.4 percent to CHF 4.7 billion in the first quarter of 2025, the Swiss Federation of Master Builders(SBV) reported in a press release. It estimates construction activity to be stable despite the international trade conflicts. For the year as a whole, the association expects construction activity to grow by 1.1 per cent year-on-year.

The SBC experts observed different developments in the individual sectors of the construction industry in the quarter under review. Commercial construction, for example, was 7 per cent weaker than in the first quarter of 2024. By contrast, construction activity in public building construction increased by 23 per cent at the same time. In civil engineering, a decline in private construction activity was largely offset by growth of 2.8 per cent in the much stronger public civil engineering sector. The bottom line is that construction activity in civil engineering fell by around 2 per cent.

In the press release, the SBC emphasises the “surprisingly” positive development in residential construction. At CHF 1.7 billion, turnover here was 2.4 per cent higher than in the same quarter of the previous year. The SBC experts consider the 11 per cent year-on-year growth in new orders observed at the same time to be “particularly pleasing”. They attribute this to the increased number of building applications in the previous year, which is now “gradually being reflected in the order books”.

The cantonal initiative “Protect affordable housing – stop vacancies” aims to control rent increases through state intervention and restrict conversions to condominiums. This would allow municipalities to introduce an authorisation requirement for renovations, conversions and changes of use. However, the cantonal government sees the initiative as problematic: “Rent caps are counterproductive in the long term,” explains Carmen Walker Späh, Director of Economic Affairs.

Experience from Geneva: a warning example The cantonal government refers to the situation in Geneva, where there are strict rent controls and authorisation requirements. There, it has been shown that new construction activity is declining significantly, while a considerable price difference has developed between existing and new rents. This regulation means that many people are staying in the same flat for a record-breaking length of time, which is exacerbating the housing shortage.

Danger for energy-efficient renovations and high-density construction The government council also sees the danger that a rent cap could reduce the motivation for important renovations and energy-efficient renovations. This could have a negative impact on the quality of living and the condition of many properties. According to the cantonal government, the planned measures also encroach on property rights and increase the administrative burden due to complex authorisation procedures.

New strategies to promote residential construction Instead of rent controls, the cantonal government is focussing on increased construction activity to relieve the market. A framework credit for cantonal housing promotion is to be doubled to CHF 360 million in order to specifically strengthen non-profit housing construction. In addition, a counter-proposal to the “More affordable housing in the canton of Zurich” initiative will further support the creation of affordable housing.

With these measures, the cantonal government is pursuing a long-term price-curbing approach aimed at combating the housing shortage through increased construction activity and targeted housing promotion. The rejection of the housing protection initiative reflects the aim of improving the housing situation without interfering with the economic freedom rights of property owners.

A study by property consultants Wüest Partner, headquartered in Zurich, concludes that residential construction activity in Switzerland will pick up in the medium term. The rise in interest rates in the years 2021 to 2023 has slowed down construction activity and thus the growth of the property stock. This has led to falling building land prices, according to a press release from the Federal Office for Housing(BWO) on the study. Building will therefore become more economical again in the medium term. In addition, the higher reference rate for rents has increased income. This is also stimulating construction activity.

The housing market is currently in a transitional phase, after which equilibrium will be restored. However, the expected increase in construction activity is likely to be lower than before the interest rate hike. In March, the Swiss National Bank lowered the key interest rate again from 1.75 per cent to 1.5 per cent.

Wüest Partner conducted the study “Rise in interest rates: effects on residential construction and prices” on behalf of the BWO. It analysed the development of interest rates and construction activity between 2021 and 2023.

The Federal Office’s statistics point to a decline in the vacancy rate, which is attributable to declining construction activity and growing population density. This leads to a significant supply gap of around 10,000 flats per year. This shortage is becoming increasingly noticeable in urban areas in particular, which emphasises the urgency of swift measures to prevent the housing shortage from worsening.

The demand for urban densification in accordance with spatial planning laws poses major challenges for property developers. Stricter regulations and an excess of bureaucratic hurdles make the construction process more complex and lead to rising costs. Appeals and lengthy legal procedures delay construction projects and increase rents.

Various measures are needed to facilitate residential construction in urban areas: Structure and utilisation plans must be revised and obstacles to densification removed. By abolishing or adapting utilisation ratios and boundary distances, more living space can be created and green spaces preserved.

Furthermore, building regulations for high-density development should be simplified. Outdated noise protection regulations, regulations on shadow impact and aesthetic regulations must be modernised or abolished. A reduction in objections and an acceleration of legal procedures are necessary in order to realise construction projects more efficiently and relieve the housing market.

One promising solution could be to simplify urban construction planning and at the same time optimise public participation in order to improve the realisation and acceptance of projects. This would not only shorten construction times, but also reduce costs and ultimately create affordable housing.

A balanced combination of economic efficiency and social responsibility is the key to the healthy development of the property market. By focussing on innovative building concepts, sustainable development practices and forward-thinking urban planning, cities can continue to grow and flourish without compromising quality of life.

Switzerland’s permanent resident population is expected to pass the 9 million mark in the first half of 2024 and could reach the magical 10 million mark by the mid-2030s. This rapid increase is historically unprecedented and is mainly driven by international migration, while construction activity cannot keep pace.

Since the rise from Switzerland’s 5 million in 1955, more housing has been created and transport infrastructure has been massively expanded, helping to keep rents rising only moderately in relation to wages. However, this era of falling housing costs, greater consumption of space per person and more comfortable living seems to be over. Due to the decline in construction activity, there could be a shortfall of at least 150,000 flats by 2034 in order to keep space consumption stable.

This is likely to result in rents rising faster than incomes. Rents on offer could rise by a total of 25 to 30 per cent in real terms by the mid-2030s, similar to the situation between 2002 and 2012. Rents in central locations in particular will rise even more sharply than in the periphery due to high immigration.

Residential property prices, whether for owner-occupied homes or multi-family houses, are also expected to rise faster than incomes at moderate interest rates. Prime locations will continue to be in high demand due to growth, and the agglomerations around the major centres will also gain in importance, which will increase the willingness to pay in these areas. Residential property could therefore build on or even exceed past increases in value.

However, there are also risks. If the housing situation deteriorates for many households, politicians could introduce additional regulations, which would exacerbate the situation. In such a scenario, construction activity could decline further and the building fabric and sustainability could suffer, as there are no incentives for comprehensive and energy-efficient renovations. The future of the property sector in Switzerland therefore depends on a balanced political and economic development.

In the first half of 2023, the main construction industry generated 11 billion Swiss francs in turnover, which is practically stagnant compared to the same semester last year. Building construction and civil engineering developed similarly. Accordingly, capacity utilisation is still high and the employment situation is good.

Lower construction activity in the medium term

In the medium term, however, the outlook is becoming gloomier. In the first half of the current year, orders in building construction were CHF 0.6 billion lower than in the same period last year, in civil engineering CHF 0.5 billion lower. Overall, this corresponds to a decline of 8.3 percent. Several companies even reported a negative order intake overall. This means that already planned construction projects were temporarily paused, redimensioned or completely put on hold.

Accordingly, the work in progress has also decreased in the past quarters, standing at 15.9 billion Swiss francs at the end of June 2023, 2.6 percent lower than a year ago.

From housing surplus to housing shortage

The stock of housing orders has also declined. The trend is clear, too few flats will be built this year and next. In the last 12 months, the franc volume of approved housing applications has fallen by 9 per cent compared to the previous 12 months. The housing shortage could be solved more quickly with less regulation. In addition, appeals are often used to push through particular interests at the expense of the creation of new housing. SBC will lobby accordingly at the Federal Council’s next round table on the housing shortage so that construction activity can be accelerated again.

SBC thanks Credit Suisse for very good cooperation – Construction Index to be continued

The Construction Index predicts a 2% increase in turnover for the next quarter compared to the same period last year. This edition marks the end of SBC’s 14-year partnership with Credit Suisse on the Construction Index. SBC would like to thank Credit Suisse for the always very good cooperation, it has been greatly appreciated. SBC will continue the established forecasting tool, from the 4th quarter of 2023 in an adapted form and with a new look.

One of the main reasons for the decline in construction activity is the complex and lengthy approval procedures. According to the ZKB study, it takes an average of 140 days from planning application to building permit in the country, which is 67 percent more than in 2010. It takes even longer in densely populated areas in particular: 500 days in the canton of Geneva and 330 days in the canton of Zurich, with this figure more than doubling since 2010. The increase in appeals and objections also lead to delays and blocked projects.

To solve these problems, the globally unique virtual reality (VR) solution from the Swiss PropTech company HEGIAS helps. Communication between the various stakeholders is improved through the use of VR, as all parties involved see and thus understand the same thing. Also, the imagination is less challenged by the authorities, and thus more correct urban planning decisions can be made.

Build faster, cheaper and more sustainably With the immersive solution, complex approval procedures can be reduced, as authorities and politicians can view the planned buildings from any perspective and at any time of day throughout the year in a realistic VR environment. This saves time, money and reduces the need for expensive and environmentally harmful façade samples or elaborate physical architectural models as well as 1:1 mock-ups.

HEGIAS VR also facilitates and speeds up the assessment of listed buildings, as for example HEGIAS VR was successfully used by Implenia in the Lokstadt in Winterthur. The VR models can also show neighbours how shadows cast or the position of the sun would affect their property at any time of day throughout the year. VR thus enables faster, cheaper and more sustainable construction.

Zug is one of the most popular economic and living areas. This is proven by numerous studies and rankings. The success is based on a long-term development strategy and attractive framework conditions. Zug offers a unique combination of excellent location factors such as the availability of skilled workers, stability, attractive taxation, central location, quality of life, level of education and economic friendliness.

The Zug business center is dynamic, as evidenced by developments on the real estate market and in the transport infrastructure. The strong presence of value-added industries and service providers as well as a high concentration of high-growth sectors are important for the quality of economic development. The broadly diversified industry structure and the unique mix of small, large, local and international companies are an important driver for the innovative development of the canton. The focus of economic management by the Department of Economics is on the existing and established companies. Their growth makes the greatest contribution to the canton's economic development.

Testimonials

Silvia Thalmann-Gut, member of the government, economics director and governor of the canton of Zug

The canton of Zug offers excellent location conditions for everyone. This includes the "Spirit of Zug" that is lived. The distances are short, the authorities work quickly and efficiently. Zug's success is based on a long-term strategy.

Heini Schmid, lawyer, former Cantonal Councilor and long-time President of Zug Tourism

Zug is in Switzerland what Switzerland is in Europe: small, surrounded by large neighbors and therefore open and adaptable. For us, changes are always an opportunity to do things differently and better. Zug is Switzerland to the power of two; it is the total package that counts.

Matthias Rebellius, CEO Siemens Smart Infrastructure, Chairman of the Board of Directors Siemens Schweiz AG

From Zug, we are driving digitalization at Siemens Smart Infrastructure. For us, Zug is an ideal location for our global headquarters, as we can attract and promote the best local and international talent here.

Johanna Friedl-Naderer, President Europe, Canada & Partner Markets, Biogen

Zug is the hub of our international headquarters. From here we coordinate our operational and administrative activities worldwide. The central location and high quality of life make Zug an attractive location for top talent.

Contact point for the economy of the Canton of Zug Welcome to the canton of Zug. Our services are aimed directly at you as an entrepreneur. We are your partner and promote Zug as a business location.

Business contact point, Aabachstrasse 5, 6300 Zug, T +41 41 728 55 04, economy@zg.ch

Alberto Diaz, Deputy Ladder; Peter Müllhaupt, jur. Employee; Yvonne Valentino, assistant / back office manager; Ursula Kottmann Müller, Marketing / Communication; Beat Bachmann, Head (from left to right). Photographer: Peter Hofstetter

Wir verwenden Cookies zur Unterstützung und Verbesserung unserer Dienste. Mit der Nutzung dieser Website erklären Sie sich mit der Verwendung von Cookies einverstanden. Weitere Informationen finden Sie in unserer Datenschutzerklärung.