Wer heute eine Immobilie an bester Lage erstehen will, braucht viel Geld und Geduld. Vor Büro- und Wohngebäuden mit hervorragender Erschliessung bilden sich heute lange virtuelle Schlangen von Investoren, die ihre Mittel möglichst sicher anlegen wollen. Bieterverfahren treiben die Preise auf neue Höchstwerte: In der Zürcher Goldküsten-Gemeinde Zumikon etwa erwarb ein Käufer kürzlich ein nicht mehr benötigtes, nur eine Minute neben einer ÖV-Station gelegenes Feuerwehrgebäude mit einigen Wohnungen für rund CHF 21 Mio. 37 Interessenten hatten sich beworben, der Endpreis lag fast zweieinhalb Mal so hoch wie der von der Gemeinde aufgrund einer professionellen Schätzung vorgegebene Mindestpreis von CHF 8.7 Mio. Im Fokus der Anleger standen 2021 vor allem sogenannte Core-Objekte: “Als risikoarme Anlageklasse sind erstklassige Immobilien nach wie vor ohne Alternative”, begründet Yonas Mulugeta, CEO von CSL Immobilien, diese in den Zentren beobachtbare Entwicklung.

Die Preisentwicklung führte 2021 dazu, dass die Netto-Anfangsrenditen in den meisten Segmenten des Investmentmarkts weiter auf neue Tiefstwerte sanken – dies, obwohl die meisten Investoren eher eine Seitwärtsbewegung erwartet hatten. Wohnliegenschaften erstklassiger Güte rentierten im Landesschnitt mit 1.85% (Vorjahr 2.1%). Noch stärker sanken die Renditen für Top-Büroobjekte: Diese fielen mit 1.9% (Vorjahr 2.35%) sogar knapp auf das Niveau der Wohnimmobilien.

Ein Grund dafür: Investoren, die im Wohnmarkt nicht mehr zum Zug kamen, wichen in den Büromarkt aus. Auf Interesse stiessen 2021 auch Gewerbe- und Logistikimmobilien – dies als eine weitere Ausweichbewegung von Investoren, die vom boomenden Onlinehandel profitieren wollen.

Leere Büros in der Peripherie

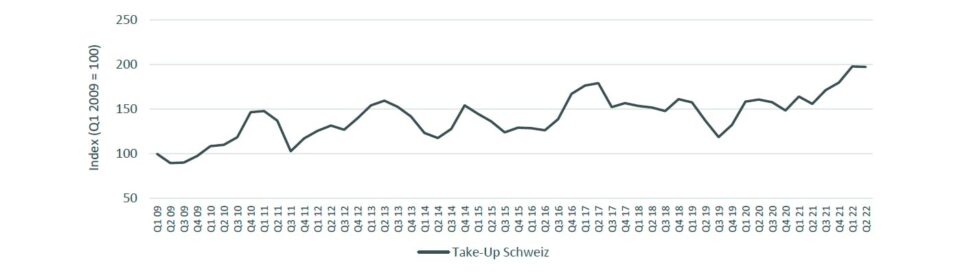

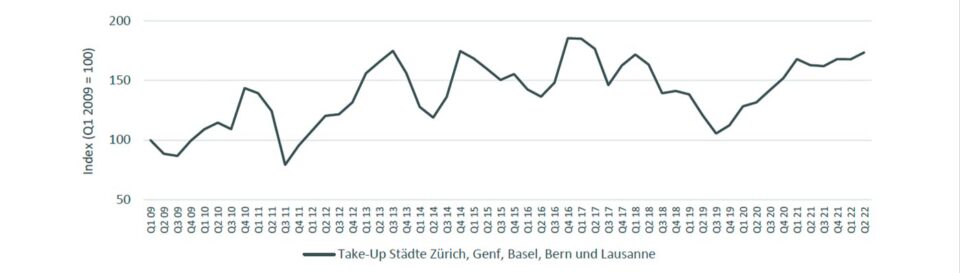

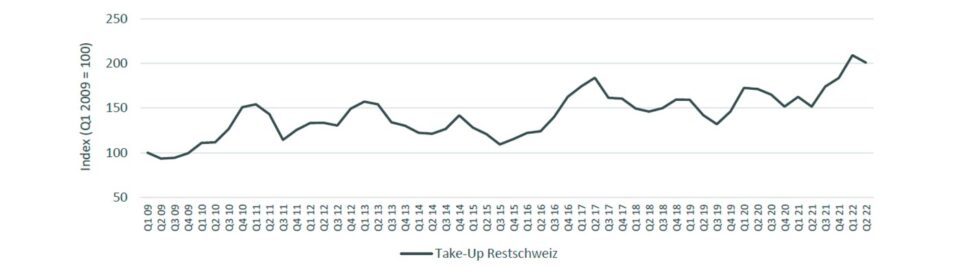

Auch die Unternehmen fokussierten ihre Nachfrage 2021 noch stärker auf zentrale Standorte. Der grössere Teil der in den vergangenen sechs Monaten verfügbaren Büroflächen von 2.43 Mio. m2 (Vorjahr 2.26 Mio. m2) entfiel deshalb auf Liegenschaften ausserhalb der städtischen Zentren. Im Wirtschaftsraum Zürich waren in den vergangenen sechs Monaten rund 910’000 m2 Bürofläche inseriert (Vorjahr 812’000 m2). Damit ist das Angebot innerhalb eines Jahres um 12% gestiegen – ähnlich stark wie in den Wirtschaftsräumen Bern (+14%) und Genf (+12%).

Der Fokus der Unternehmen auf zentrale Bürostandorte ist insbesondere auch auf die Pandemie zurückzuführen. Viele Mitarbeitende haben sich an das Homeoffice gewöhnt. Um sie zumindest teilweise zurück ins Büro zu holen und dort einen neuen Alltag zu etablieren, muss dieses attraktiv sein. Neben der zentralen Lage mit guter Verkehrsanbindung gehört dazu ein ansprechendes Interieur, das Kreativität und Teamprozesse fördert. Unternehmen, die dies nicht bieten können, haben auf dem Arbeitsmarkt einen Nachteil.

Eigenheimpreise flächendeckend gestiegen

Auch im Wohnmarkt machte sich die Pandemie bemerkbar: Das Zuhause gewann an Bedeutung. Gleichzeitig löste das Homeoffice in vielen Haushalten ein Platzproblem aus. Dies führte zu einer steigenden Nachfrage – insbesondere im Eigentumssegment, das weiterhin vom attraktiven Finanzierungsumfeld profitiert. Auf der Angebotsseite kam nur wenig Neues hinzu. Die Folge waren fast flächendeckend steigende Preise für Eigenheime. Dieser Trend dürfte sich 2022 fortsetzen – die Hypothekarzinsen bleiben auf tiefem Niveau, auch wenn sie zuletzt leicht gestiegen sind.

Im Mietwohnungssegment wirkte sich die gestiegene Nachfrage insbesondere strukturell aus: Gesucht waren 2021 vor allem grössere Objekte, während das Interesse an 1- bis 2.5-Zimmer-Wohnungen an vielen Lagen spürbar abnahm. Die Erfahrung von CSL Immobilien im Markt zeigt: Paare beziehen heute kaum mehr eine 2.5-Zimmer-Wohnung, sondern suchen mindestens eine Wohnung mit 3.5, lieber noch mit 4.5 Zimmern. Dies zeigt sich auch in den Zahlen: Im Kanton Zürich stieg der Anteil der 1- bis 2.5-Zimmer-Wohnungen unter den leerstehenden Wohnungen 2021 auf 27%, ein Jahr zuvor lag dieser noch bei 22%.

Die Leerstandsquote im Wohnmarkt sank 2021 aufgrund der grossen Nachfrage über das ganze Land gesehen auf 1.54% (Vorjahr 1.72%).

Allerdings zeigt die Quote grosse regionale Unterschiede. Im Vergleich der grössten Agglomerationen weist Zug mit 0.4% den tiefsten Wert auf, Olten-Zofingen mit 3.8% den höchsten. Im Kanton Zürich lag die Leerstandsquote 2021 bei 0.72% (Vorjahr 0.91%). In der Stadt Zürich stieg die Leerstandsquote 2021 zwar minimal an, zeigte aber mit 0.17% (Vorjahr 0.15%) immer noch einen äusserst ausgetrockneten Markt.