As of the end of June, office space available across Switzerland within three months rose for the second consecutive quarter to 1.67 million sqm, or 3.5% of the stock (see Figure 1), after reaching a multi-year low of 3.2% in Q4 2022. This is mainly due to an additional supply of office space in the suburbs of Zurich (airport region and Limmattal), where the availability rate rose from 15% to 16.6% within the six-month period. On Zurich city land, office supply also rose to 190,000 sq m or 2.8%, 13,000 sq m more than in Q1 2023 (177,000 sq m or 2.7%) and the first increase since Q4 2020 (see Figure 2). Especially in Zurich’s CBD (Central Business District), supply increased by 8,000 sqm to 51,000 sqm (2.6 %) within three months.

In Zurich, it is noticeable that some companies in the information and communications technology (ICT) sector, which accounted for a large share of demand in recent years, have reviewed or revised their expansion plans. In addition, the merger of the two largest Swiss banks, UBS and Credit Suisse, will also gradually have an impact on the Zurich office market. Although this impact is not expected to be significant, it could create good opportunities for other market participants to find centrally located space in a still tight market environment with low construction activity and upward pressure on prime rents.

Furthermore, it is noticeable that the increase in available office space in the city of Basel has turned into a reduction in supply for the first time since 2016. Some major leasing successes in the CBD and Klybeck have led to a reduction in the availability rate from 5.6% to 4.5% (117,000 m2) within one quarter. However, a significant rebound in supply is expected in the medium term.

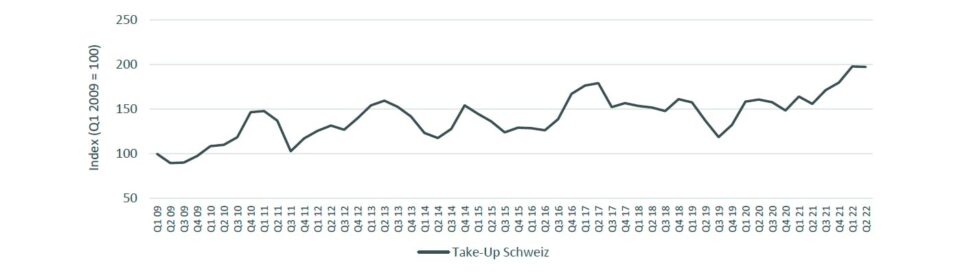

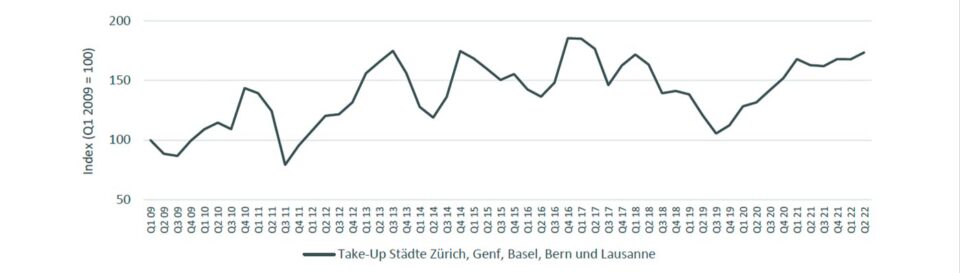

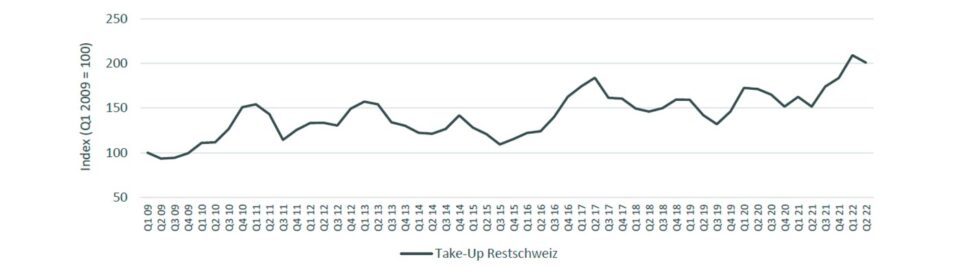

Otherwise, the office space markets in the other Swiss cities of Geneva, Bern and Lausanne are proving stable and thus unimpressed by the slowdown in economic growth. The Swiss office market has benefited from high take-up in recent years, with good economic growth even more than offsetting the impact of home working. However, office demand has recently slowed due to the weakening economy, and subletting activity has also increased. Office take-up in the first half of 2023 is down 28% from the first half of 2022 to an average of 490,000 sq m per quarter and is expected to remain at this lower level in the second half of 2023, which is roughly in line with the long-term average (see Figure 3).