According to the survey of 432 real estate professionals, interest in property is increasing in almost all market segments. Single-family homes in particular are seeing an increase in demand, which is already above the 2024 level. Condominiums and apartment buildings also remain in demand, while the number of available properties is decreasing.

The imbalance between supply and demand is leading to a relative shortage, the impact of which varies from region to region. This is most pronounced in densely populated central cantons and growth regions.

Building land and new construction as bottlenecks

The high demand for building land illustrates the growing pressure on future construction activity. Over half of those surveyed reported increasing interest in plots of land, but in most regions there is a lack of sufficient building land ready for planning.

At the same time, construction activity remains too weak to even come close to meeting demand. High construction costs, lengthy approval procedures and a lack of land are dampening momentum. This is structurally exacerbating the supply shortage. A phenomenon that has been apparent for years.

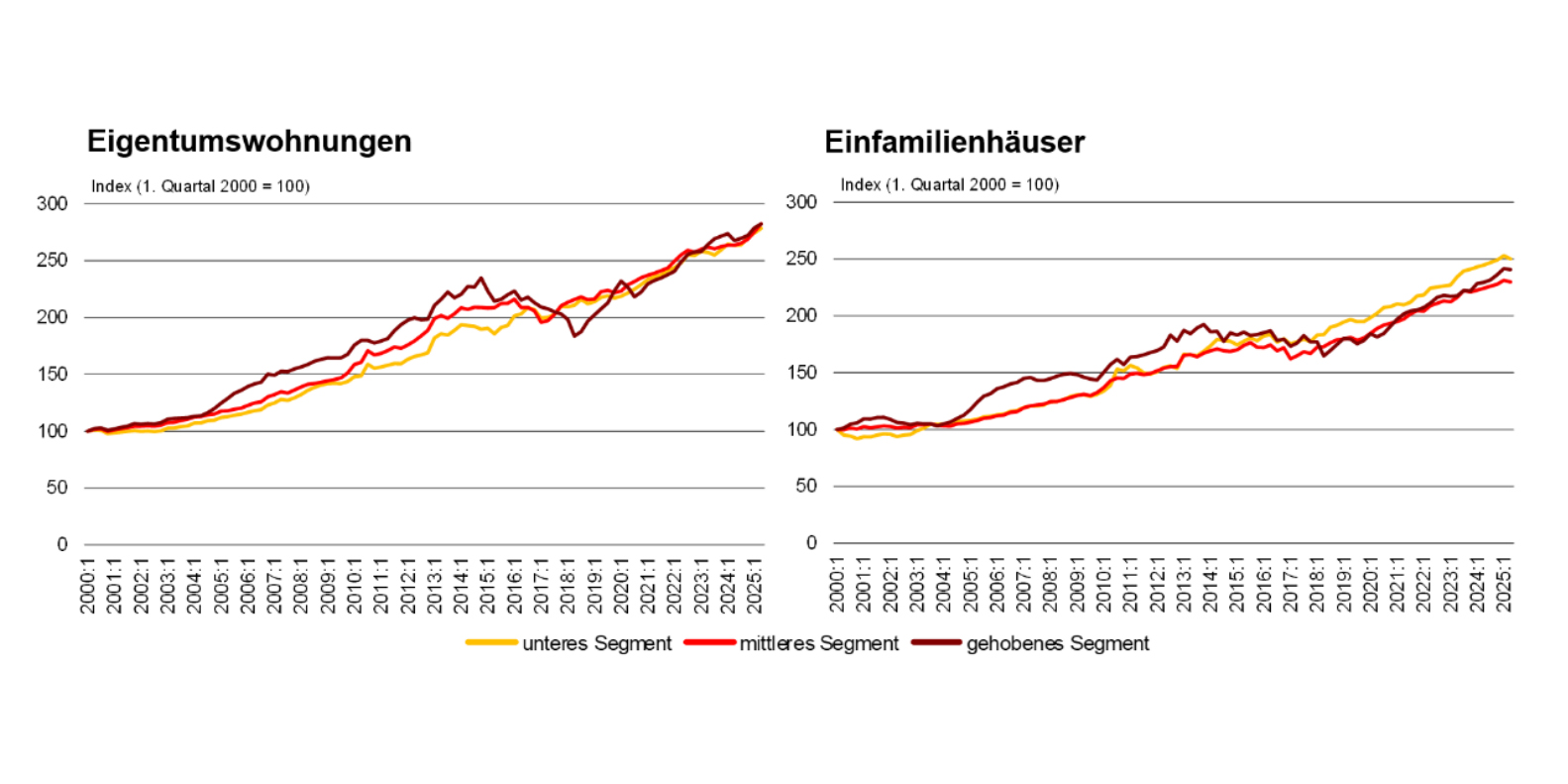

Price pressure continues

Three quarters of those surveyed expect prices for residential property to continue to rise in the coming year. The combination of low new construction activity, persistently high demand and political and regulatory hurdles is creating an environment in which price adjustments are becoming the norm. For many buyer households, owning a home is increasingly becoming a math problem, especially as interest rate trends are placing an additional burden on financing.

Structural stress test for the middle class

Restricted access to home ownership has a long-term impact on the social structure. For decades, home ownership has been a central pillar of wealth accumulation and retirement provision in Switzerland. If this access is systematically made more difficult, the financial prospects of broad sections of the population will shift, with potential effects on consumer behavior, choice of location and family planning.

Political and planning levers

HEV Switzerland is therefore calling for clear political steps to break through the structural delay. Simpler approval procedures, shorter planning periods, less bureaucracy and effective measures against abusive objections. New housing supply can only be created if the regulatory framework is reliable and investment-friendly.

A market at a turning point

The survey makes it clear that the real estate market is at a crucial point in 2025. While demand remains robust and confidence in home ownership is unbroken, the structural shortage is jeopardizing the balance of the system. Without a correction, the price spiral threatens to become entrenched, with consequences for entire generations of prospective buyers.

The coming years will show whether politicians, planners and market players can reverse the trend or whether the bottleneck will become the new normal in the Swiss real estate market.