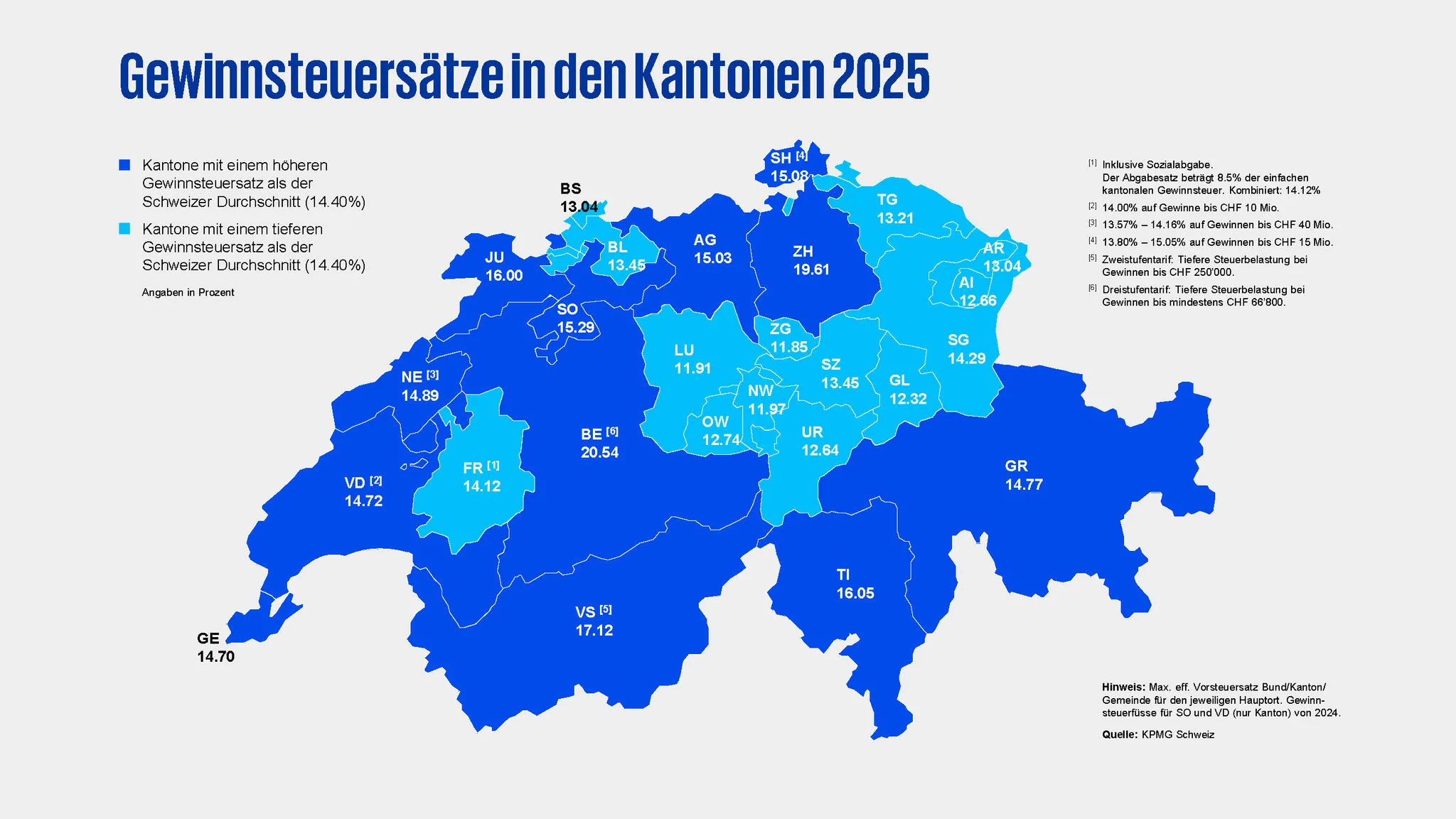

In 2025, the average corporate income tax rate in Switzerland fell from 14.6% to 14.4%. The canton of Zug remains the front-runner with just 11.85%, while Bern (20.54%), Zurich (19.61%) and Valais (17.12%) occupy the upper ranks in the tax ranking. At first glance, this is a sign of the attractiveness of the business location, but the dynamics are more nuanced.

In fact, some cantons have even increased their tax rates slightly. Geneva, for example, rose from 14 to 14.7 percent, while Basel-Stadt will increase its rate to 14.53 percent in 2026. This is due to the introduction of the global minimum tax rate of 15% for companies with high profits. Cantons that were previously regarded as low-tax locations are adapting in order to cushion the threat of the additional tax and retain revenue themselves. For investors, this means that while the tax advantage remains, flexibility is required in order to be able to react to cantonal differences and future adjustments.

Location remains competitive

There has also been a slight decrease in the top tax rates for private individuals. From an average of 32.7 percent to 32.5 percent. Geneva (-1.7 percentage points) and Schwyz (-0.61) in particular have lowered their rates. However, the ranking remains stable. Schwyz (21.98%), Zug (22.68%) and Nidwalden (24.1%) remain at the top. Geneva, Vaud and Bern remain the most expensive cantons for top earners. For real estate developers and highly skilled workers, these locational differences in income tax remain a decisive factor, especially for international projects.

Global minimum tax Stability in Switzerland, uncertainties internationally

Over 50 countries worldwide have already implemented the minimum tax of 15 percent for large companies. However, the USA, the original driving force behind the initiative, has not yet adopted the OECD guidelines into national law. On the contrary, the new US administration is increasingly questioning the project. Experts such as Stefan Kuhn from KPMG Switzerland emphasize that, in the worst-case scenario, these uncertainties could lead to a return of tax competition or special digital taxes. For Switzerland, however, the signal is clear: the global minimum tax is becoming a reality here too. The stability of implementation and the ability to plan remain a locational advantage over uncertain international developments.

Cantons boost location attractiveness with targeted projects

In parallel to the tax adjustments, many cantons are investing in location promotion projects. Lucerne, Basel-Stadt, Zug and others have already adopted programs to support local companies and new relocations. For real estate developers, this means opportunities for new projects, incentives for investment in commercial and residential space and a solid basis for long-term viable business models.

At the same time, it is clear that it is not tax policy that determines the attractiveness of a location, but also the accompanying measures such as infrastructure, securing skilled workers and digitalization. This is where new spaces for innovative projects are created for developers and investors,

especially in a market environment that is characterized by growing demands for sustainability and resource efficiency.

Industrial policy and tariffs

In addition to taxes, international trade issues are once again gaining in importance. Discussions about US tariffs, bilateral trade agreements and strategic industrial policy are driving reindustrialization worldwide. For Swiss locations, this means that the demand for suitable production and logistics space could increase. At the same time, the protection of strategic industries is once again receiving greater political support, which could open up new areas for investment in high-tech and industrial production.

Switzerland remains strong – eyes on Ireland and Asia

In an international comparison, Switzerland remains on a par with other top European locations. Ireland taxes corporate profits at 12.5 percent, Hungary at 9 percent. Guernsey, the Bahamas and the Cayman Islands remain low-tax havens with zero percent, but this is no comparison for Switzerland. Instead, the location competes with attractive metropolises such as Hong Kong (16.5%) or Singapore (17%), which entice with additional incentive programs. China, India and Brazil also continue to rely on other tax strategies with high rates (25-34%), but selectively offer low effective burdens for strategic industries. Switzerland remains competitive and complements this advantage with a stable political and legal framework.