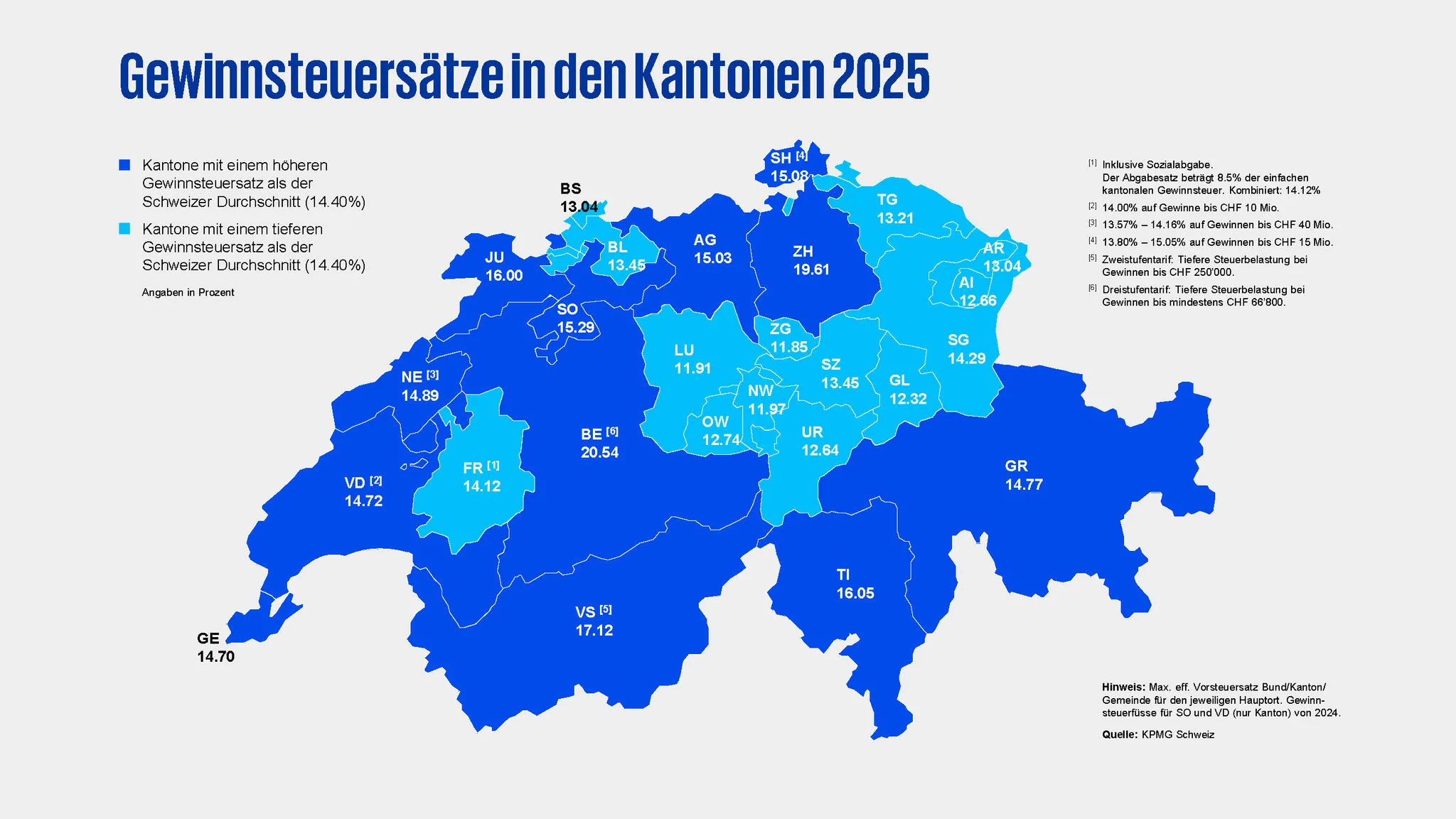

Lucerne is lowering its effective corporate tax rate from 11.91 to 11.66 per cent in 2026, overtaking Zug, which is now at 11.71 per cent. According to PwC, this makes Lucerne the canton with the lowest corporate tax rate in Switzerland for the first time.

The difference is small, but the message is all the greater. In tax competition, it is not only the absolute amount that counts, but also the symbolic effect. Whoever is at the top sends a clear signal to mobile companies and investors.

Switzerland keeps moving

Eight cantons are lowering their corporate taxes slightly, while four are increasing them minimally. Overall, the 2026 tax comparison shows a country that remains active in international competition and does not simply manage its attractiveness.

It is striking that the OECD minimum tax introduced in 2024 has hardly changed the cantonal tax rates so far. PwC speaks of a rather wait-and-see attitude towards the new global framework conditions. This is precisely why competition within Switzerland continues to gain in importance.

Zurich and Bern are coming under pressure

At the other end of the scale are Bern and Zurich. According to PwC, Berne has an effective rate of 20.54 per cent, while Zurich is still at 19.47 per cent despite a slight reduction. Both cantons therefore continue to be among the most expensive locations for companies in Switzerland in terms of taxes.

This is tricky from a location perspective. After all, high economic quality, good accessibility and strong labour markets are not always enough if the fiscal difference is almost twice as high as in Lucerne. The tax factor remains a tough lever in the competition for new relocations and expansions.

More than just a tax ranking

According to PwC, Central Switzerland maintains its role as a particularly attractive business location. In an international comparison, Lucerne and Zug rank at the lower end of the tax burden; in the EU, only Hungary taxes companies more heavily than Lucerne.

This makes it clear what is really at stake. It’s not just about a difference in figures between two cantons, but about the strategic positioning of entire economic areas. Lucerne has taken a small step towards the top. This is precisely what can make the difference in the competition between locations.